Managing the Risks of an Ageing Workforce

Rachel Pu

Asia Head,

Workers' Compensation

At the heart of underwriter insights

Older workers approaching or at retirement age already represent a significant proportion of Asia’s workforce. Yet most employers are unaware of the novel risks they present to business.

Much continues to be said about Asia’s ageing population. People are living longer, while birth rates remain stubbornly low. Better medical care and healthier lifestyles are driving the former, while career and lifestyle choices, as well as a high living costs, are mostly behind the latter.

In Asia, the proportion of the workforce aged 65 or older is already high. In several markets, about one-in-five are aged within this group. By 2050 — just 25 years from now — this number will rise to between 30% and 40% in these same markets. It is therefore imperative that employers understand the needs and preferences of this demographic. And critically, are fully aware of the potential challenges these workers both face and present to their employers.

Very few business know the proportion of older workers they employ however, nor are they unaware of the different risk profile people approaching or in retirement create. Accordingly, few have workplace policies and practices that cater to the needs of this age group. That most employers are unaware of these facts is somewhat alarming: employers are expected by both the authorities and employee families to ensure their workers maintain good health and wellbeing; and in the event that they become injured, businesses do their best to help them return to work as soon as possible, with a focus on alternative, less stressful duties, especially for older workers.

The ensuing whitepaper outlines the scale of matter across five Asian markets: Hong Kong, Malaysia, Macau, Singapore and Vietnam. It highlights the physical and psychological traits typically associated with ageing; and articulates how different injuries and illnesses can negatively impact business operations. The paper offers solutions to better manage these different risks.

It should be noted that older employees also bring many benefits to the workplace. The paper explores how business can capitalise on the experience and know-how presented by this group as well.

As an insurer, our role is simple — to create risk awareness and provide practical advice to employers, so that workplace health and safety concerns can mitigated, and incidents prevented.

Our Rapidly Ageing Workforce

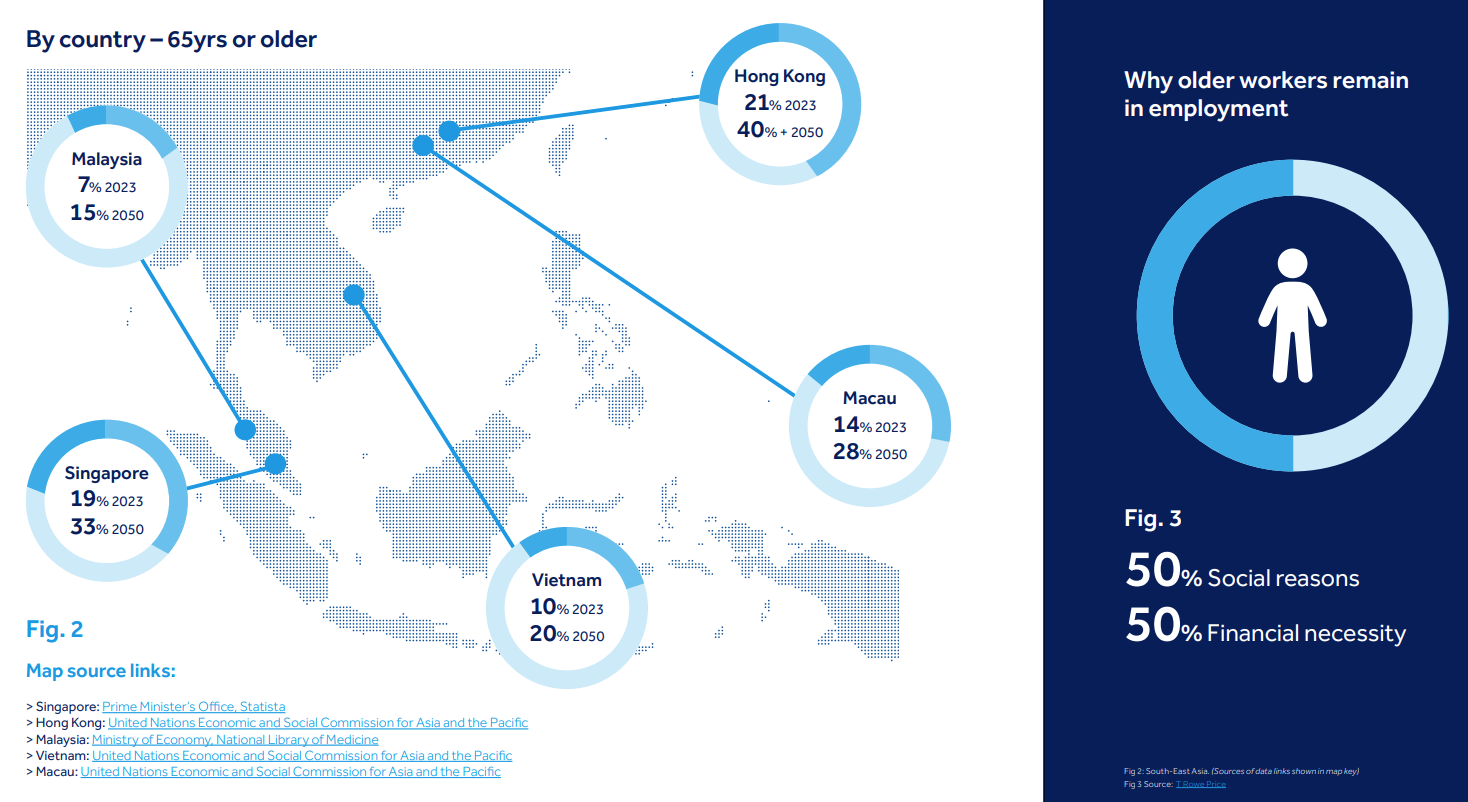

In many countries across Asia, the amount of people aged over 65 is noteworthy. In Singapore, the proportion of the population aged 65 or older was about 19% in 2023. By 2050, this will rise to 33% — one-third of the city state’s citizens. The situation in Hong Kong is more acute. Those within this age group represented over 21% of the population in 2023, yet by mid-century it will increase to over 40% of the population, meaning that almost one in two persons will be of retirement age by then.

Few countries are bucking the trend. In Malaysia, the proportion of people aged 65 of over was over 7% in 2023; by 2050 it will double to 15%. It’s a similar story in Vietnam and Macau, where these proportions will grow from about 10% and about 14% respectively, to 20% and over 28% accordingly.

Such expansion will have a profound impact on economies, where retirement ages are already being raised. Various nations around the region are incapable of supporting this age group through social welfare alone, and are relying on their working populations to provide for the elderly. However, as the proportion of people at retirement rapid proliferates, there is a need for this age group remain in employment.

Studies suggest that almost half of those who remain in work do so out of necessity. Today’s cost of living is frequently cited as a key driver behind this trend. In 2015 for example, global inflation and consumer prices rose just 1.5% year-on-year. In 2022, they rose 8% annually. Furthermore, most state retirement plans have not kept in line with inflation, prompting retirees to seek supplemental income. A 2023 study found that 70% of Asia-Pacific workers remain employed due to financial concerns.

Not everyone remains in work solely for money, however. Many work because they find it rewarding, as well as an opportunity to learn new skills and enjoy new experiences. Others see it as a means of avoiding boredom and loneliness. While some work to enjoy the benefits they will receive while being employed, including insurance.

Despite the enormity of this topic at both national and company levels, few business leaders are aware of exactly how many members of staff are over the age of 65 or approaching retirement. Nor are they cognizant of how this demographic changes the risk profile of their companies. In our experience, a small proportion of business leaders are able give a close estimate of these numbers, yet the overwhelming majority have no idea what these are. As such, they are underprepared and underinsured for the risks they are exposed to.

Business should therefore prepare for both the risks and opportunities this new paradigm presents to business operations, including its workforce, workplace health and safety (WHS) practices, and productivity, among other factors.

Common accidents and illnesses

Ageing affects the body and mind in many ways. Most importantly, the ageing process impacts individuals differently. Research finds that there are multiple ways ageing can impact the brain. Some of the more common traits include memory loss; the inability to multitask; and a decrease in attention spans. Yet other research finds older adults have the ability to learn new skills, form new memories, and improve vocabulary and language skills.

Individuals also physically age at different speeds. Studies confirm that over time, our response times slow, we tire more quickly and have less physical strength, and are more vulnerable to illnesses than those younger than us — yet overall, these hindrances evolve uniquely in people. Likewise, the elderly generally take longer to recover from accidents and illnesses than their younger colleagues, while recovery times vary enormously. As such there is a no-one-size-fits-all understanding to how people age.

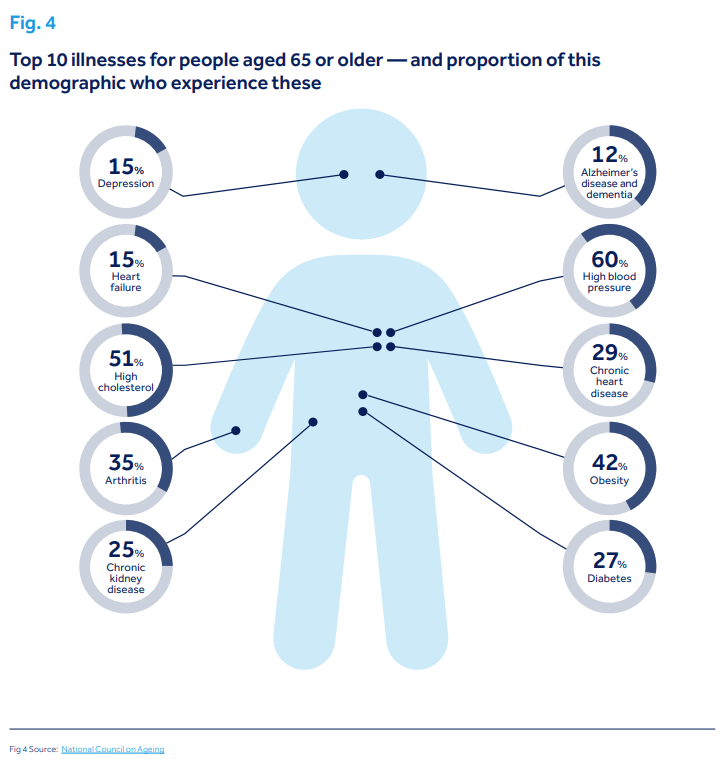

Vulnerability to illnesses is a noteworthy concern. Those approaching or above retirement age are prone to a wide range of diseases. Some 60% of adults aged 65 or older experience high blood pressure, which can cause dizziness, fatigue and mood swings. Over 50% of this age group have high cholesterol, which increases the likelihood of heart disease, stroke and other problems.

A further 42% of this demographic are obese, which can make workers less productive, and more prone to absenteeism due to associated illnesses diabetes, cardiovascular disease, and musculoskeletal disorders. Meanwhile, more than one-third have arthritis, which can severely impair our ability type, grip a pen, hold a phone to our ear, or carry out manual work.

Workers aged 65 or older aren’t just more vulnerable to physical illnesses. Depression impacts 15% of this age group, which can severely impact focus, decision making and time management, as well as social interactions, and communication. And 12% of this demographic are diagnosed with Alzheimer’s disease, where they struggle to remember practices and recall the critical knowledge needed to execute various tasks — potentially leading to lowered productivity and increased WHS risks.

How can businesses better cater to an increasingly older workforce, to ensure that their evolving risk profiles are mitigated, while making sure that the opportunities brought about by this age group are capitalised upon?

Preparing for a new paradigm

While governments across the region are increasingly rolling out policies and laws to better support an ageing workforce, it is the private sector that will drive the measures needed to better cater to this age group.

As with many new initiatives, knowing where to commence is a key challenge for most organisations. Conducting an audit of employees by age is a good place to start. This will immediately give employers an understanding of the age profile of their workforce, and indicate how this might evolve in future. They should also consult with older employees, including those over retirement age or approaching this, in order to understand their future work plans. Knowing just how many people are within this age bracket will enable employers to ascertain their risk profile, and enable them to implement policies and procedures accordingly.

Businesses must also assess the suitability of roles for older workers — it may be that a position involves heavy lifting for example, which means that there is a higher risk of injury if carried out by an older worker; while others might involve the manning of machinery, which demands fast reflexes should it faulter. Businesses have a responsibility to ensure that all employees are in good health, irrespective of age; they must also support return to work, which in the case of many older workers, will involve alternative, less stressful duties.

Overall, employers should think about how their business operates, and how older workers can add value, including support improvements to WHS practices. This might involve older workers mentoring younger colleagues in a structured programme to share their knowledge and experience. Indeed, moving older workers away from known risks is also an opportunity: skilled workers are typically able to pass on their knowhow to younger employees, or can assist with other functions that are less demanding physically.

It is also important to avoid assumptions about the capabilities of, or strain on, older workers. As reiterated earlier, no two workers age the same. Management must therefore consult with them when considering elderly-friendly policies and measures — certain jobs that are physically demanding should not automatically preclude an older worker. Businesses should also consider whether technology can play a part to alleviate physical strain as well.

New policies and practices

Older workers typically have abilities and experience that are different to their younger colleagues. Yet typically companies implement a one-size-fits-all approach to how they manage their employees. As the proportion of older workers grows within workforces, employers must therefore consider new measures that cater to this age group. Such policies should not only ensure that older workers are able to perform their roles with minimal risk of injury; they should also make sure they are content within the company.

Careful consideration is needed when planning these. There is a chance that measures catering to workers aged over 50 for example, may be seen as discriminatory or exclusive to those in their 20s and 30s. As such, engagement with all age groups is necessary when considering any such measures.

A further concern is retrenchment. Dismissing an employee because of their age might be illegal, depending on local laws. Plus, employers could very well lose intellectual property (IP) as well as key skills, which are not easily replaceable, in the event that they suddenly end a worker’s employment. If a particular role isn’t deemed suitable, there is the opportunity to upskill these workers into new roles, through training and development.

There is also the livelihood of older workers to contemplate. Many are reliant on employments to fund their daily outgoings and lifestyle preferences. Furthermore, a large proportion of workers have had to change careers, either because their past roles are now unsuitable to their physical abilities, or that opportunities in their chosen profession have become limited.Venturing into new roles further underscores the need to view older workers a little differently than the rest of the workforce.

Measures catering to an older workforce may include granting those aged 65 or above additional days of leave; allowing them extra break time; or providing gym membership to help them stay fit, among others. Businesses should appoint a senior manager to champion age-friendly practices, and ensure that the views of this segment of the workforce are represented to company management.

Offering flexible work arrangements will not only be well received by this age group, they also enable companies to attract talent that may not be available to work between certain hours due to other commitments. Policies that look after different age groups tend to be viewed favourably by Millennials and Gen Z especially, and can be used as a selling point to attract top talent from these younger workers.

Role of insurance companies

While insurers like QBE are in the risk transfer business, they nonetheless have a role to play in helping employers prevent the accidents and illnesses, which often impair older workers.

Specifically, they can support employees get back to work as soon as possible when injured, and can advise on measures to keep workforces healthy, both physically and mentally. They therefore can play a critical role in ensuring business continuity, and proliferating a sense of positivity across the workforce that is critical to boosting productivity.

There is also an opportunity to contribute beyond the provision of risk services. There are many such services that are outside of insurance yet influence risk. Through connections within the business community, the industry’s contribution might involve helping to facilitate discounts on gym memberships for example; or it could help businesses source counselling services and other third-party experts, which in turn will help maintain a healthy workforce.

Insurers are also able to advise on the latest government policies that impact workforces, interpret how these might impact employers, and where need be, suggest insurance policies and solutions to meet these statutory requirements. Despite mandatory schemes such as Hong Kong’s Employees Compensation Insurance, and Singapore’s Work Injury Compensation, knowledge of how these work in practice on the part of company leadership, especially those running small and mediumsized businesses, may be limited.

Ultimately, it is the role of insurers to make business leaders aware of the many risks that they face — including those associated with an older workforce — and help their companies steer clear of these.

Capitalising on the opportunity

Older workforces can bring enormous amounts of experience and know-how to their employers, adding value in areas that younger workers may not be able to realise. By employing the former, it is also an opportunity for companies to build a more inclusive workforce that brings together different ways of thinking and problem solving. Where possible, employers should upskill older workers to ensure they are performing roles that are easily within their physical abilities, while keeping critical IP within the business.

Employing older workers does create a different risk profile however, to one that employs younger manpower. Accordingly, businesses should understand what these risks are, and should explore ways to prevent these.

Businesses should therefore:

- Know the number of employees approaching or at retirement age; and understand their future plans at least one year out from this, in order to make contingency plans, if necessary.

- Consider less physically demanding roles for these employees. Where necessary provide training and development to upskill them to more suited positions.

- Support older workers with activities and programmes that ensure they are in good health, physically and mentally.

- Help those, who may have become injured or contracted an illness, to return to work as soon as possible, by connecting them with support services, whether internally or externally.

- Speak to QBE to understand the different risks associated with older workers, and the types of solutions that can help transfer this risk.